Tactical asset allocation using blotter

NOTE: If you simply want to test strategies in R, please see the post: Tactical Asset Allocation Using quantstrat. quantstrat uses blotter behind the scenes, but provides a higher level of abstraction.

blotter is an R package that tracks the P&L of your trading systems (or simulations), even if your portfolio spans many security types and/or currencies. This post uses blotter to track a simple two-ETF trading system.

The contents of this post borrow heavily from code and comments in the “longtrend” demo script in the blotter package. Many thanks to Peter Carl and Brian Peterson for their hard work.

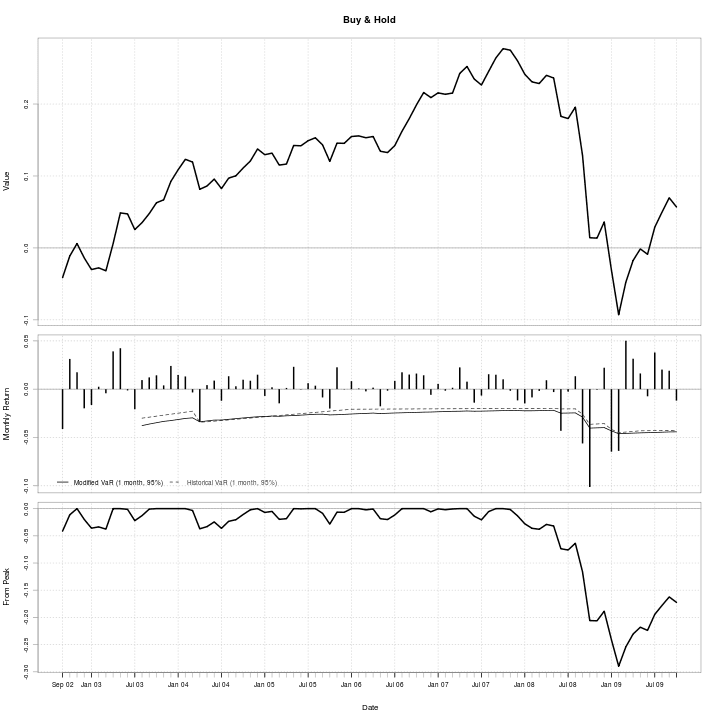

The first chart shows the result of holding an equal-weight portfolio of SPY and IEF from 2002-07-31 to 2009-10-31. The 2008 bear market led to a 30% drawdown in this portfolio.

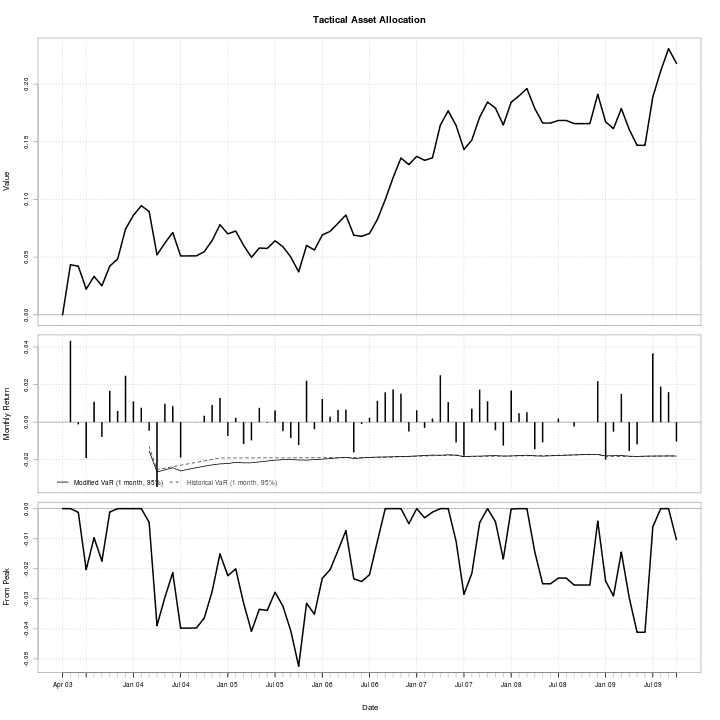

The second chart shows the result of following Mebane Faber’s tactical asset allocation approach using the same ETFs and time period. Though it did not perform as well as buy-and-hold through 2007, the 2008 bear market only caused a 5% drawdown for this strategy. Both observations are consistent with the conclusion in Faber’s article.

Without further ado, here’s the code:

# This code implements the strategy found in:

# Faber, Mebane T., "A Quantitative Approach to Tactical Asset Allocation."

# Journal of Risk Management (Spring 2007).

# The article implements a simpler version of the 200-day SMA, opting for a

# 10-month SMA because monthly data are more easily available in earlier

# periods and lower granularity should translate to lower transaction costs.

# The rules of the system are relatively simple:

# - Buy when monthly price > 10-month SMA

# - Sell and move to cash when monthly price < 10-month SMA

# 1. All entry and exit prices are on the day of the signal at the close.

# 2. All data series are total return series including dividends, updated monthly.

# NOTE: For the purposes of this demo, we only use price returns.

# 3. Cash returns are estimated with 90-day commercial paper. Margin rates for

# leveraged models are estimated with the broker call rate.

# NOTE: For the purposes of this demo, we ignore interest and leverage.

# 4. Taxes, commissions, and slippage are excluded.

# Data:

# This demo uses monthly data downloaded from Yahoo Finance for two ETFs: SPY and

# IEF. These were chosen to illustrate the classic stock/bond asset portfolio.

# Though longer serires would be preferred, data for IEF begin in mid-2002.

# Load required libraries

library(quantmod)

library(TTR)

library(blotter) # r-forge revision 193

library(PerformanceAnalytics)

# Make sure system timezone is "UTC"

Sys.setenv(TZ = "UTC")

# Clean up in case the code was already run in this session

try(rm("account.default","portfolio.default",pos=.blotter),silent=TRUE)

# Set initial values

initDate='2002-07-31'

endDate='2009-10-31'

initEq=100000

# Set currency and instruments

currency("USD")

stock("IEF",currency="USD",multiplier=1)

stock("SPY",currency="USD",multiplier=1)

# Load data with quantmod

print("Loading data")

symbols = c("IEF", "SPY")

getSymbols(symbols, from=initDate, to=endDate, index.class=c("POSIXt","POSIXct"))

# Adjust prices for splits/dividends (thanks pg)

#IEF = adjustOHLC(IEF)

#SPY = adjustOHLC(SPY)

# Convert data to monthly frequency (to.weekly() needs drop.time=FALSE)

IEF = to.monthly(IEF, indexAt='endof', drop.time=FALSE)

SPY = to.monthly(SPY, indexAt='endof', drop.time=FALSE)

# Set up indicators with TTR

print("Setting up indicators")

IEF$SMA = SMA(Cl(IEF), 10)

SPY$SMA = SMA(Cl(SPY), 10)

# Set up a portfolio object and an account object in blotter

initPortf(name='default', symbols=symbols, initDate=initDate)

initAcct(name='default', portfolios='default', initDate=initDate, initEq=initEq)

verbose = TRUE

# Create trades

for( i in 10:NROW(SPY) ) {

CurrentDate=time(SPY)[i]

equity = getEndEq(Account='default', CurrentDate)

for( symbol in symbols ) {

sym = get(symbol)

ClosePrice = as.numeric(Cl(sym[i,]))

Posn = getPosQty(Portfolio='default', Symbol=symbol, Date=CurrentDate)

UnitSize = as.numeric(trunc((equity/NROW(symbols))/ClosePrice))

# Position Entry (assume fill at close)

if( Posn == 0 ) {

# No position, so test to initiate Long position

if( Cl(sym[i,]) > sym[i,'SMA'] ) {

# Store trade with blotter

addTxn('default', Symbol=symbol, TxnDate=CurrentDate,

TxnPrice=ClosePrice, TxnQty=UnitSize, TxnFees=0, verbose=verbose)

}

} else {

# Have a position, so check exit

if( Cl(sym[i,]) < sym[i,'SMA'] ) {

# Store trade with blotter

addTxn(Portfolio='default', Symbol=symbol, TxnDate=CurrentDate,

TxnPrice=ClosePrice, TxnQty=-Posn, TxnFees=0, verbose=verbose)

}

}

} # End symbols loop

# Calculate P&L and resulting equity with blotter

updatePortf(Portfolio='default', Dates=CurrentDate)

updateAcct(name='default', Dates=CurrentDate)

updateEndEq(Account='default', Dates=CurrentDate)

} # End dates loop

# Buy and Hold cumulative equity

buyhold = exp(cumsum( ( 0.5*ROC(Cl(IEF)) + 0.5*ROC(Cl(SPY)) )[-1] ))

# Final values

cat('Tactical Asset Allocation Return: ',(getEndEq(Account='default', Date=CurrentDate)-initEq)/initEq,'\n')

cat('Buy and Hold Return: ',tail(buyhold,1)-1,'\n')

# Plot Strategy Summary

png(filename="20091118_blotter_strategy.png", 720, 720)

charts.PerformanceSummary(ROC(getAccount('default')$summary$End.Eq)[-1],main="Tactical Asset Allocation")

dev.off()

# Plot Buy and Hold Summary

png(filename="20091118_blotter_buyhold.png", 720, 720)

charts.PerformanceSummary(ROC(buyhold)[-1],main="Buy & Hold")

dev.off()

If you love using my open-source work (e.g. quantmod, TTR, xts, IBrokers, microbenchmark, blotter, quantstrat, etc.), you can give back by sponsoring me on GitHub. I truly appreciate anything you’re willing and able to give!